19

May 2015If You had Sex in the Back Seat … Would Your Insurer Know?!

Ever since the Internet of Things became a thing, the tension between telematics and privacy has been on some people’s minds. As it turns out, fitness monitoring devices have the potential to share, oh, so much more than you’d assume.

Ever since the Internet of Things became a thing, the tension between telematics and privacy has been on some people’s minds. As it turns out, fitness monitoring devices have the potential to share, oh, so much more than you’d assume.

Does your fitness monitoring device kiss and tell?

We’re talking about the wearable devices that track lifestyle activity throughout the day, calculating just how many steps you take, calories you burn and foods you consume.

Now that this type of data is available, life and health insurance providers have an opportunity to harness it, offering customers personalized rates in exchange for wearing one of the devices in question.

In Johannesburg, for example, customers can share lifestyle metrics with insurers via fitness monitoring devices, earning points for healthy habits. The same service may be coming soon to the United States. It won’t be long before you could reel in a lower life insurance rate by letting your insurer track your health through a wearable device.

Not everyone’s excited about that idea, of course.

Kashmir Hill, Fusion contributor and senior editor at Fusion’s Real Future, has a concern and she spells it S-E-X. “First, insurance companies gave us black boxes to put in our cars so they could track our driving, in exchange for discounts when we refrain from speeding,” Hill wrote. “Now, they’re coming for our bodies.”

How much does your insurer know about your sex life?

Hill is referring to a funny TechCrunch article posted by Gregory Ferenstein, who inadvertently discovered that his sexual activity registered a recognizable pattern on his health-tracking watch – one that’s noticeably different from the patterns produced by his other activities, including yoga, weight-lifting and grocery-shopping.

“Were I married, my wife might like to know why I burned 100 calories between 1:07 to 2:00 a.m., without taking a single step, and fell asleep right afterwards,” Ferenstein wrote.

This observation didn’t bother him one bit. “For techno-optimists (like myself), radical transparency in sex is a welcome part of life: it will reduce cheating and prompt honest conversations about satisfaction,” Ferenstein said. “For techno-pessimists, it opens a can of worms (no pun intended) that people would sooner keep closed.”

Hill ,whose personal mission is “to prove privacy isn’t dead yet,” is presumably on the “techno-pessimist” side of Ferenstein’s coin. Either way, it’s clear that fitness monitoring devices are capable of divulging some pretty personal data with whomever is on the other end.

In auto insurance, we spell it UBI – not TMI.

While health and life insurers who connect their offerings to telematics data may end up knowing more about your personal habits than you meant to share, rest assured, auto insurers will not be listening in. What happens in the back seat stays in the back seat.

That’s because the data that UBI is based on is concerned with your car’s behavior – not your own. So, unless your sex life happens to affect your braking, cornering, speed or garaging location, your auto insurer will never be the wiser.

Contact us to learn more and subscribe to our e-newsletter for more usage based insurance updates.

14

May 2015Beyond Discounts: How to Differentiate Usage Based Insurance

It started with just a few innovative brands, changing the way insurance was done. But now, usage based insurance has taken the industry by storm. ABI Research projected that telematics subscriptions will make a mind-blowing leap from 5.5 million in 2013 to 107 million in 2018.

As a result, what was once a novel disruption is rapidly becoming a core offering, and brand differentiation is the word of the hour. Yesterday, customers were asking, “Do you offer usage based insurance?” Tomorrow they will want to know, “What makes your usage based insurance different?”

Brand differentiation in insurance telematics

Just about every usage based insurance program delivers a discount for good driving – that’s the fundamental value proposition of insurance telematics. However, to differentiate, an insurer must go beyond that.

How? According to an Epsilon infographic:

- 27.5 percent of telematics customers want a good driver discount.

- 25.1 percent want reward points and gift certificates from a UBI program.

- 57.4 percent want both.

“Consumers want to be recognized and rewarded for their loyalty and the money they spend with brands,” Epsilon Contributor Dave Edington said. “They also expect leading brands to present more relevant and personalized offers in exchange for the data they provide.”

The loyalty quotient

Based on their experiences in other industries, consumers may expect more from insurance than just insurance. To truly differentiate, insurers may need to build in personalized rewards, such as car wash coupons or other offers relevant to the driver’s geographical location.

Deloitte University Press suggests the following usage based insurance differentiators:

- Immediate feedback on driving safety

- Road condition alerts

- Roadside assistance facilitation

- Identification of lost or stolen vehicles

- Geo-fencing to allow electronic monitoring of a child or elderly parent’s location and driving behavior

Gamification is another potential point of connection and reward:

“Insurers could provide rewards for improvements in driving behavior, relative to their own performance as well as against the broader policyholder pool, certain segments, or even specific groups of individuals,” Deloitte University Press contributors said. “Insurers could thereby use telematics to make the customer experience more interactive, competitive, gratifying, and perhaps even fun—certainly not an attribute traditionally associated with insurance.”

The data is there. Now it’s a question of how to harness that data in a meaningful way to strengthen the bond between customer and brand. The answer will require creativity, but those brands that put in the brainstorming effort now will reap the benefits.

While the exact formula for differentiation is yet to be determined, one thing is for certain: As an efficient, agile, and wildly-popular communication tool, the smartphone is uniquely suited as a vehicle capable of achieving UBI differentiation. To learn more, download our free report, “10 Reasons to Unplug and Unburden UBI.”

06

May 2015Noteworthy Takeaways from New Study on UBI Telematics

The National Association of Insurance Commissioners (NAIC) recently released their latest study with the Center for Insurance Policy Research (CIPR). The topic? Usage based insurance of course.

The purpose of the new study, “Usage-based Insurance and Vehicle Telematics,” was to examine how UBI has changed the face of the auto insurance, from the impacts of telematics on the market to its implications for insurers, consumers and regulators alike. Below are key highlights.

New benefits, new risks.

The auto insurance industry “is undoubtedly undergoing a fundamental change,” the study said, resulting in more efficient risk-pricing and broad benefits to just about everyone involved. PHYD pricing “promises to benefit individuals, insurance companies and the country as a whole.”

Wait a minute. How could the whole country benefit from usage based insurance? Here’s one example: Simply giving consumers an incentive to drive fewer miles could result in the following societal benefits:

- Individuals are empowered to reduce their premiums.

- CO2 emissions fall.

- Traffic decreases.

- Fewer collisions improve public health.

- The nation’s dependence on oil becomes less acute.

At the same time, insurers that avoid bringing UBI telematics into their core offerings end up shouldering an unnecessary burden, “as companies failing to do so face fairly extreme adverse selection risk,” the study said.

It’s easy to see their point. Why would safe drivers who travel fewer miles at low risk times want to continue paying rates that reflect the average risk rather than their own risk? Why would safe teenagers want to continue paying exorbitant rates? Once UBI awareness increases, budget-savvy, safe drivers will rapidly migrate to UBI policies.

What role do smartphones play?

“Smartphones are an ideal telematics solution as they are typically equipped with a host of relevant sensors, such as GPS, accelerometers and gyroscopes,” the study said. “They also have large data storage capacity, or infinite with the cloud, and superior communication abilities.” Furthermore, they aren’t encumbered by hardware device or installation costs.

A few additional highlights.

The 86-page study covers a great deal of information, including telematics modeling and analytics, market observations, economic considerations, consumer concerns and regulatory implications. That said, here are a few quick takeaways.

- Most of the survey respondents (89 percent) said that UBI is available in their jurisdiction of the United States.

- California, New Mexico, the Virgin Islands, Puerto Rico and Guam lag behind in that regard.

- For regulators, data transparency is a crucial prerequisite to letting telematics programs into their areas.

- Smartphone telematics apps include features that make UBI programs more transparent.

- The main benefit for insurers is the ability to develop more accurate risk assessment and pricing.

To learn more about UBI in the auto insurance industry, read the report. To find out how smartphone UBI can transform your insurance business, click here.

28

Apr 2015The Insurance Telematics Disruption: How to Survive the Big One

It’s coming. Experts have studied it. The question isn’t if, but when.

It’s coming. Experts have studied it. The question isn’t if, but when.

We’re not talking about a major natural disaster that may or may not occur sometime in the future. No, we’re talking about a change that’s making waves right now – the insurance telematics disruption known as UBI.

Already, usage based insurance is changing the industry landscape. “Most of the top 10 auto insurers have UBI programs,” Insurance Journal said. “According to Progressive, more than 1.6 million drivers have signed on to use its Snapshot product since 2008.”

But a big wave is only trouble for those who aren’t prepared to ride it. Here are three tips to help you survive the big one.

1. Understand the magnitude of the disruption. Just as experts study timelines, plates and magnitude to assess the impact of a coming quake, insurers must evaluate just how intense the telematics disruption is going to be. “IoT has only started to affect P&C insurance, but the situation is rapidly changing,” Property Casualty 360 contributors said last month. “A recent Strategy Meets Action study reveals that nearly a quarter of insurers are in some phase of IoT deployment. Broad scale IoT deployment such as usage based insurance (UBI) and other telematics solutions imply limitations to premium growth as discounts proliferate.”

Case in point: Snapshot users have increased from 20 to 35 percent in just two years. This isn’t an isolated incident. It’s an industry-wide transformation. As Strategy Meets Action put it, “Any company with a stake in the personal auto insurance business must recognize that usage based insurance (UBI) is a market disrupting force that will have a major impact over the next 10 years.”

2. Identify how imminent the disruption is. “To prepare your response and time your move, it’s key to estimate when these events will affect you,” Nicholas Evans, contributor to ComputerWorld, said in an article on technological disruption. “Is this something you need to act on immediately or something you should continue to monitor closely? Either way, it’s good to have a strategic plan and weigh all the response scenarios.”

Again based on SMA research, Insurance Journal summarized that “70 percent of North American property/casualty insurers are operating or planning UBI programs, and 75 percent believe UBI will ‘fundamentally alter the auto insurance industry between now and 2020.” That’s a mere five years away. Long enough to roll out smart, strategic changes. Not long enough to dawdle.

3. Build a survival plan you can count on. Preparing for a physical quake involves a range of preparations, from the simple (like bolting down your bookshelves) to the strategic (like making seismic upgrades to a structure). The same goes for industry disruptions. In the case of insurance telematics, the action plan is straightforward. It’s time to make usage based insurance one of your core offerings.

Wondering if you should go with smartphone UBI or OBD-based UBI? Our comparison chart helps break down the differences. Get it here.

22

Apr 2015Who Drives Better, Men or Women?

That old saying about “women drivers” seems to have gone the way of the dinosaur – at least among insurance companies. It’s no secret that men pay more for their premiums. It’s no accident, either.

That old saying about “women drivers” seems to have gone the way of the dinosaur – at least among insurance companies. It’s no secret that men pay more for their premiums. It’s no accident, either.

According to traditional insurance data, male drivers are more likely to get into severe collisions, resulting in pricier claims; hence the bigger premium that men pay when they get behind the wheel. But how accurate is traditional insurance data? Is it really true that women have won the driving badge in the battle of the sexes?

Traditional data says risk calculation is about quality, not quantity

It’s not that women make fewer mistakes than men – it’s that they make different mistakes.

In other words, women get in plenty of car accidents. But according to traditional insurance data, these are more likely to be fender-benders. Men, on the other hand, engage in riskier behaviors more often, such as speeding, not wearing seat belts, and driving under the influence. As a result, when men get in a wreck, they tend to get, well, wrecked.

“No messing around here: When men are at the wheel, crashes are more likely to end in totaled cars, costly medical bills, and well-fed lawyers,” Bloomberg Business wrote.

Here’s how the Insurance Institute for Highway Safety broke it down for 2012:

- Of the driving fatalities, 71 percent were male

- Of fatally-injured male drivers, 38 percent had a breath-alcohol content of over 0.08 percent

- Only 20 percent of fatally-injured female drivers did

- Of male drivers involved in fatal accidents, 23 percent were speeding

- Only 14 percent of female drivers were

Usage based insurance data adds a bit more insight to this picture

So are women better drivers? An infographic based on UBI data would say yes. After looking at “154 million miles of data over 40 million journeys and 19 thousand customers,” Wunelli found that compared to men, women:

- Exceed the speed limit 12 percent less

- Hit the brakes hard 11 percent less

- Drive on roads they know 7 percent more

- Drive 5 percent less overall

- Drive 28 percent less at night

Behavior-driven insurance: Attract better drivers with a fairer deal

In the past, drivers with a high risk profile just had to wait it out. Conventional wisdom was simply to keep up the good work and trust that over time, that premium will probably go down. Other pieces of advice have included choosing a conservative vehicle, building good credit, looking for “good driver” and “good student” discounts – and finally, price-shopping.

Pay-how-you-drive insurance puts a better option on the table. When a driver opts for usage based insurance, they can significantly shorten the time it takes for their price tag to reflect their behavior. For those who don’t fit their stereotype, that’s a huge draw.

No insurance company wants its best drivers to go hunting for a better deal because they’re disgruntled by rates they feel they don’t deserve. With PHYD insurance, they don’t have to.

Want to receive more great info about all the future of usage based insurance? Subscribe to our e-newsletter here.

20

Apr 2015Mobile App Engagement: New Study Provides Roadmap

Are you engaging your customers successfully with mobile apps? If you’re like most brands, the answer is no. That’s what a recent Forrester report suggests. “In 2015,” Forrester wrote, “marketing leaders who have embraced the mobile mind shift will accelerate spending to create an insurmountable gap between themselves — the industry leaders — and the laggards who view mobile as just another channel.”

Are you engaging your customers successfully with mobile apps? If you’re like most brands, the answer is no. That’s what a recent Forrester report suggests. “In 2015,” Forrester wrote, “marketing leaders who have embraced the mobile mind shift will accelerate spending to create an insurmountable gap between themselves — the industry leaders — and the laggards who view mobile as just another channel.”

Introducing the “mobile mind shift”

What’s a mobile-shifted marketer? One who leverages mobile to transform customer experience and drive business outcomes. Mobile-shifted marketing will be the crucial trend in 2015. Meanwhile, treating mobile as “just another channel” is rapidly becoming a dinosaur mindset.

That doesn’t mean we won’t be seeing a lot of dinosaurs. “Success stories will be few in number,” Forrester predicted.

Three ways to improve mobile engagement in 2015

- Rethink everything. We’re living in what Forrester calls “the mobile moment.” Mobile is possibly the most disruptive business technology since the Internet: It’s “forced businesses to completely rethink how they win, serve, and retain customers.”

- Give them what they want. This “mobile moment” boils down to what customers expect from the brands they engage with. They want the info, services and perks they’re looking for, in context, the moment they need them. To date, 18 percent of U.S. consumers already think this way, while another 30 percent are moving that direction. That’s just in the U.S. The mobile mind-shift is happening across the world.

- Deliver experiences. U.S. and UK consumers may use 24 apps on average, but they divide 80 percent of their time among just five of those. They have app fatigue: the volume of available apps is plain overwhelming, so they’ve narrowed it down to those that are most useful. Brands that are sensitive to this will focus on delivering experiences, not just info and services, and they’ll make them as seamless as possible.

How big is this going to get?

The scale of the mobile shift is fairly remarkable. Forrester observed that companies with lots of mobile users are “being acquired for astounding valuations,” while the most successful apps for customer engagement globally are being developed into platforms which stand to rule the mobile world.

These platform companies are pouring funds into tracking customer engagement and spending, aiming to crack the code on what makes apps work for consumers. “Observing behavior across so many phones offers unique opportunities to spot trends or early demand for products — or lack thereof,” Forrester wrote.

All told, businesses that want to stay competitive will need to re-engineer their approach “to deliver valuable mobile moments” to their customers.

How to begin? Check out this list from the media, events and research company StreetFight for ideas, and pay attention to point #6, “Enhance the user experience in real time.” See this article for more info on why real-time UBI calculation is a non-negotiable.

To learn more about integrating mobile with your insurance offerings, check out our OBD vs. Smartphone UBI comparison chart.

14

Apr 2015Insights: Why Auto Insurance Customer Satisfaction Has Dropped

The American Customer Satisfaction Index (ACSI) – an independent benchmark based on annual surveys – says satisfaction is down 3 percent in property and casualty insurance. Website CustomerRespect.com reports that GEICO and Progressive took the hardest hit among individual carriers.

The American Customer Satisfaction Index (ACSI) – an independent benchmark based on annual surveys – says satisfaction is down 3 percent in property and casualty insurance. Website CustomerRespect.com reports that GEICO and Progressive took the hardest hit among individual carriers.

Why the recent drop in customer satisfaction? A recent Market Insight Group report, sponsored by Applied Systems, provides some clues about the customer expectation disconnect. The report looks at what’s essential to customer experience, now that we live in an online digital mobile society. It’s founded on the idea that customer interaction today isn’t what it used to be.

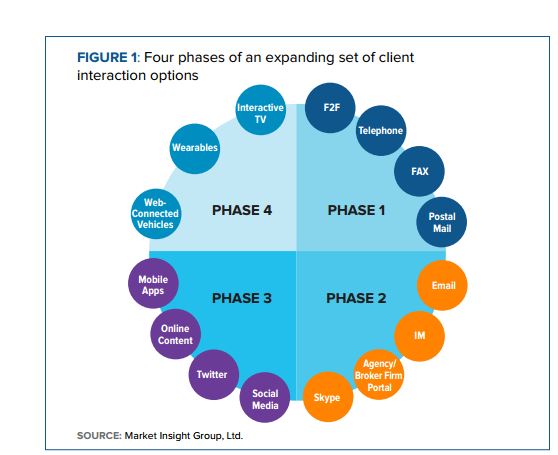

Property Casualty 360 summarizes the report findings as follows: Over the past 20 years or so, the channels of engagement have evolved in four distinct phases.

- To imagine phase one, think back to when communication happened exclusively via phone, fax and the postal system, if it wasn’t happening face-to-face.

- Phase two introduced email and instant-messaging to that picture.

- Phase three ushered in social media, online content and mobile apps.

- In phase four, we look forward to an era of web-connected vehicles and wearable devices.

While phase four is still just emerging, it’s important to note that phase three “is rapidly becoming the ‘new normal’ of online digital communication,” according to the firm’s assessment.

Yet – counterintuitively – the report suggests that customers still expect to interact with their insurers primarily face-to-face or through email.

In other words, customers don’t expect their insurance providers to offer the level of experience they’ve grown to rely on in every other customer interaction they engage in. That is not a recipe for satisfaction.

Customer retention for the win

Bottom line, insurers need to build mobile apps, social media and other digital channels into their customer engagement efforts – and they need to do it fast. As we’ve said before, it boils down to customer experience. How can insurers be more accessible and deliver more value through relevant and frequent interactions?

Usage based insurance provides a channel to raise the customer experience bar on multiple counts. By leveraging mobile apps to deliver services via policyholder smartphones, insurers gain a way to continually reach out, seek feedback and make recommendations – following the example of giants like Amazon who’ve made themselves a model of successful customer engagement.

Want to know more about smartphone UBI? Download our complimentary report, “10 Reasons to UNPLUG and Unburden UBI.”

09

Apr 2015Auto Insurance Fraud Update

Last month, the Insurance Information Institute published a summary of recent developments in insurance fraud. So, we decided it’s time for an update.

Last month, the Insurance Information Institute published a summary of recent developments in insurance fraud. So, we decided it’s time for an update.

What’s new in auto insurance fraud according the report?

Across the industry, fraud accounts for about 10 percent of all property/casualty losses. (For auto insurers, it can get as high as 20 percent.) That puts the annual price tag for industry-wide fraud at $32 billion.

Auto insurance is one of the lines considered most vulnerable. But that’s not news to insurers. A FICO survey in 2013 showed that one in three insurers don’t feel adequately protected, especially where premium leakage and new applications are concerned.

For example, some policyholders deliberately underestimate their annual mileage, knowing that the real number would amount to a higher premium. Or they give a false zip code, because they want to be charged based on a neighborhood where rates are cheaper.

This type of fraud alone costs auto insurers roughly $16 billion a year according to the same Insurance Information Institute report.

The role anti-fraud tech can play

A report last fall by the Coalition Against Insurance Fraud underscored the importance of technology in fighting fraud – especially given that the problem is on the rise.

“Insurers are investing in different technologies to combat fraud, but a common component to all these solutions is data,” said Stuart Rose, Global Insurance Marketing Principal at SAS. “The ability to aggregate and easily visualize data is essential to identify specific fraud patterns.”

The Coalition’s study found that “the right mix of tools and technologies” can up your fraud-detection rate and make a significant dent in your overall losses.

Technology brings another benefit as well: At a time when insurance crime is on the rise, and claims and anti-fraud professionals are hard to find, tech “can help bolster these often-understaffed teams.” Even if you’re not understaffed, the right technologies can leverage investigator efficiency exponentially.

Boost your fraud-detection with usage based insurance

Insurers who’ve added usage based insurance to their offerings don’t need to worry quite so much about premium leakage and application fraud. That’s because usage based insurance delivers some of the data that the Coalition identified as crucial to cutting down your losses.

Usage based insurance data can:

- Show driving routes

- Reveal day and night-time garaging addresses

- Report miles driven and whether those miles are driven during daytime, nighttime or rush time hours

- Suggest the presence of an unreported driver in the household

- Corroborate a policyholder’s claim

In fact, in the effort to drive down insurance fraud, you could say that UBI is a lie detector. For more information on how usage based insurance serves both you and your policyholders, get the Driveway Fact Sheet.

03

Apr 2015Auto Insurance Digitization: Is Your Company Behind the Times?

It’s no secret that digitization brings the potential to transform the auto insurance industry from the ground up. For one thing, it can expand an insurer’s service offerings. According to the Bain brief, “For insurance companies, the day of digital reckoning” some carriers are leveraging mobile apps to let their customers add a vehicle, get a quote, file a claim or pay bills.

It’s no secret that digitization brings the potential to transform the auto insurance industry from the ground up. For one thing, it can expand an insurer’s service offerings. According to the Bain brief, “For insurance companies, the day of digital reckoning” some carriers are leveraging mobile apps to let their customers add a vehicle, get a quote, file a claim or pay bills.

When an insurer manages to “integrate disparate channels into a seamless experience,” as Bain said, it clearly benefits the customer. But it also benefits the company.

How digitization can optimize your business processes

Cognizant, a company specializing in business optimization, keyed into telematics as a major opportunity to boost efficiencies in auto insurance. In their words, usage based insurance is “laying the foundation for better decisions and core business process optimization.”

How? When an insurer integrates telematics into its core systems, including “policy administration, actuarial and underwriting, billing and claims, as well as new action-oriented policyholder portals,” it can achieve “more predictive and faster decisions … perhaps even in real time.” Meanwhile, manual work and time-intensive tasks “can be streamlined or eliminated as processes are automated with accurate geo-spatial and vehicle data.”

The result, Cognizant said, is a “noticeable impact on loss ratios,” with additional, quantifiable savings continuing to roll in, as insurers continue to collect and analyze UBI data.

Why are auto insurers falling behind?

Digitization isn’t just creating new efficiencies for auto insurers. It’s transforming business processes for industries across the board, from healthcare to finance. But as the news site Shanghai Daily pointed out last month, while “the financial sector is racing to embrace digital technology to boost sales and drive profits, the traditionally staid insurance industry is in danger of falling behind.”

If you were to rate your company on a scale of one to 10, how fully have you leveraged mobile technology to optimize your business processes?

Two benefits: business efficiencies, customer retention

Usage based insurance doesn’t just bring the potential to improve efficiencies; it can also improve customer retention – which stems in part from lower premiums, as well as a closer customer relationship. “That’s the Holy Grail for insurers,” Deloitte University Press said, “establishing brand stickiness by offering ongoing value to policyholders beyond the price charged for coverage and claim service provided.”

The other side of the retention coin is, interestingly enough, inconvenience. When a customer would have to cancel online bill-pay for their insurance provider and then set it up all over again with a new organization, for example, it could deter them from switching carriers in the first place, unless they were seriously disgruntled.

Bottom line, “most executives recognize that they’re on the threshold of a once-in-a-generation opportunity to both reduce costs and foster new streams of profitable revenue growth,” Bain said, speaking of digitization. And UBI telematics is a central component of that opportunity.

Want to learn more about smartphone UBI? Download our Fact Sheet.

31

Mar 2015Teen Driving Safety … Can Smartphone UBI Help?

In the Portland area, three teen drivers were recently killed in motor vehicle accidents, all in the timeframe of one weekend. These deaths have sparked a conversation among Oregon policymakers about teen driving.

In the Portland area, three teen drivers were recently killed in motor vehicle accidents, all in the timeframe of one weekend. These deaths have sparked a conversation among Oregon policymakers about teen driving.

The existing rule requires teens to go through an extended period of supervised driving before they’re fully licensed. For eight years after it was introduced, the policy brought teen crashes down by almost 30 percent. Now, however, it seems to have “reached the limits of its ability to reduce serious crashes on the roads,” Troy Costales of ODOT said.

What’s being done about it?

Legislators are talking about toughening the guidelines on when teens are allowed to have other teenagers in the car. According to a AAA study, the risk inflates by about 44 percent when a teen is driving with one other person under 21 years old. With two under-age passengers, it doubles. With three or more, it more than quadruples.

Even without any passengers, the risk is high to begin with. The ODOT teen driving manual says that for drivers age 20 and under, the crash rate has been twice as high as for the general population. “Teens have the highest crash rate of any group in the United States,” AAA said.

What else can policymakers do? Costales said they’re thinking about upping the minimum driving age to 17 or 18, or possibly restricting the driving hours for teens even further – although these ideas won’t work if they create a hardship for Oregon’s rural communities.

Can UBI driver coaching help?

While in this example, the teen driving accidents took place in Oregon, these kinds of tragedies occur throughout the nation, every day.

Maybe one aspect of the answer is already in most teens’ pockets. Smartphone telematics apps reward good driving with an insurance discount, offering drivers an incentive to improve their skills. For teens, that’s probably not much of a motivation if their parents are footing the insurance bill. However, gamification is.

If the smartphone UBI app features real-time driving data calculation, teens can receive feedback on their driving at the conclusion of every trip. When your smartphone detects every time you brake or corner too hard, and when you know you can improve your score with every incident-free trip, suddenly following the rules becomes fun. Immediate feedback makes learning easier. And when the game is safety, everyone wins.

To learn more about improving safety for teens on the road, take a look at Impact Teen Drivers: a national nonprofit founded by the mother of a teen who died in a crash.

To learn more about adding smartphone UBI to your product line up, download our OBD v. Smartphone UBI Comparison Report.