19

Feb 2015Insurance Technology: Go Digital or Go Home

The news is out. Insurers who want to grow are going digital.

The news is out. Insurers who want to grow are going digital.

A 2014 survey by Accenture suggests that digital startups related to the insurance industry are prime takeover targets by carriers, and in fact, this type of acquisition is emerging as a key strategy for insurance carriers to jump-start their digital capabilities, Insurance & Technology reports.

This news might be surprising given that insurance is a conservative industry, not generally known for innovation. In the words of one article by Deloitte University Press, “… there are those who would argue that the link between insurance and innovation is so tenuous as to be nearly nonexistent. In the words of the old cliché, innovation and insurance are only found together in the dictionary.” However, despite these stereotypes the same article goes on to prove that innovation has always been crucial to success within the industry.

That’s true now more than ever, as businesses seeking to deliver new value by harnessing digital technology – Accenture calls them “digital transformers” – small companies with big ideas to help them unlock the potential for digital. This is an area where, historically, insurers have been weak. “Only 22% [of C-level insurance execs] said investments made by their organization are focused on driving truly disruptive innovations,” Insurance & Technology reports.

How can a smaller insurer go digital without breaking the bank? By deploying insurance telematics.

Speaking of truly disruptive innovations, usage-based insurance brings “the potential to upend the stable model that has dominated the industry for more than 50 years,” according to a white paper by A.T. Kearney, entitled, “Telematics the Game Changer – Reinventing Auto Insurance.” Here’s how:

- It reinforces relationships with customers, enhancing retention. Drivers who get usage based insurance through smartphones, for example, enjoy frequent touch-points with their providers, strengthening their relationship to the brand.

- It makes claims processing more efficient. With a smartphone at the scene, drivers can begin the claims process more quickly by contacting their provider without delay; they can also take photos of any damage.

- It builds a better profit model. Ultimately, usage based insurance improves a company’s profitability, as better drivers self-select for this type of insurance. And, with built-in incentives, it can improve driver behavior over time.

Digital innovation not only sets a trend for the industry, but protects your company’s position within it. With a profitable business, greater efficiency, minimized claims and a strategy for retaining your best customers, your organization can be disruptive in the best possible way.

Usage-based insurance is just one example of the innovation you need for survival at a time when big companies are looking to acquire smaller ones. Put usage based insurance at the core of your strategy, and take advantage of the benefits it brings. To learn more about our UBI pilot program, available to select insurers, contact us.

17

Feb 2015Usage Based Insurance: Helping Senior Drivers Stay Safe

As reported by the Insurance Institute for Highway Safety, the U.S. Census Bureau predicts there will be 57.7 million adults reaching age 70 by the year 2030, more than double the 23 million recorded in 2012. Baby boomers are continuing to live and drive longer than ever before. This translates into 30 percent more drivers aged 70 and older on our roadways and the number keeps rising.

As reported by the Insurance Institute for Highway Safety, the U.S. Census Bureau predicts there will be 57.7 million adults reaching age 70 by the year 2030, more than double the 23 million recorded in 2012. Baby boomers are continuing to live and drive longer than ever before. This translates into 30 percent more drivers aged 70 and older on our roadways and the number keeps rising.

Some states are concerned that more senior drivers will equal more traffic fatalities and accidents and are creating plans to address the driving issues of our aging population. National Highway Traffic Safety Administration five-year plan includes addressing roadways and driving license restrictions.

Surprisingly, it turns out that senior driving practices are not as risky as previously believed and, in fact, some major insurance carriers even offer premium discounts to seniors. Another Insurance Institute for Highway Safety’s report in 2014 indicated that senior drivers have fewer crashes and are less likely to be injured or killed than middle-aged drivers ages 35-54 for the following reasons:

1) Seniors drive less often and for shorter distances

2) Seniors tend to avoid inclement weather conditions and night driving

3) Seniors tend to self-limit their driving if they experience limitations in their health or vision

4) Seniors are the most experienced drivers, making them safer on the road than younger drivers

Adult Children Concerned About Senior Parents Driving

Among adults whose parents are senior drivers, more than 55 percent are anxious about their parents driving habits and safety on the road. Seniors themselves are concerned about their capacity, although they want to continue driving well into their 80s. Quality of vision or hearing, impairment by medications and certain diseases such as diabetes or arthritis, memory loss, and reflex response time are all factors.

According to Liberty Mutual, seniors are willing to have “the talk” about their driving competence with their families but the discussion actually takes place only about 23 percent of the time. USAToday

The Center for Disease Control and the National Highway Traffic Safety Administration are addressing concerns about traffic safety through public education and outreach. AAA provides no-cost driver self-evaluations to help seniors identify and remedy any areas of concern and identify risk factors before there is an accident. Rather than give up the keys entirely, these programs are designed to help seniors and their families make good decisions about when it’s time to stop driving. Studies indicate that age is not the factor which should determine when an individual should stop driving. Multiple factors must be evaluated on a case-by-case basis, including vision, cognition, fitness level, strength and the impact of diseases and/or medications on driving capacity.

Senior Drivers Are a Virtually Untapped Market

Since the majority of current UBI insureds are under 34 years old, auto insurance carriers have a unique opportunity to tap into a new market segment by pushing the benefits of usage based insurance to seniors and their adult children.

User Based Insurance data would help seniors accomplish the following:

• Study driving habits to identify trouble spots and map out alternate routes that minimize risk

• Provide “proof” of safe driving habits and patterns, alleviating concerns

• Alert seniors and their families if their driving is putting themselves and/or others at risk

• Open a conversation between seniors and their adult children about driving readiness

• Raise awareness for seniors about their driving strengths as well as their risky habits

Making seniors safer drivers not only improves public safety and their quality of life, it reduces their liability as insureds, an attractive bonus to carriers. There are potentially 23 million more drivers that will need to be insured during the next 15 years, making them a great potential market for usage based insurance. Want to learn more? Download our smartphone UBI vs. OBD UBI comparison sheet.

12

Feb 2015New Alliance Helps Insurers Develop Usage Based Insurance Strategies

Today, we bring you a guest post from Roosevelt Mosley at Pinnacle Actuarial Resources. As many of you might have seen in our recent press release, we recently joined forces with Pinnacle to offer auto insurers more comprehensive usage based insurance services.

Today, we bring you a guest post from Roosevelt Mosley at Pinnacle Actuarial Resources. As many of you might have seen in our recent press release, we recently joined forces with Pinnacle to offer auto insurers more comprehensive usage based insurance services.

Usage Based Insurance Continues Steady Growth

Usage based insurance (UBI) is not only firmly established in the private passenger automobile insurance market, but is gaining market share and is here to stay. Many of the major insurance companies have launched a UBI program, and dozens of other companies are in various stages of strategy development, research, pilot programs and roll-out. Latest estimates place the market share of customers in a UBI program at 10%. Given the number of programs currently available, and those still in development, the number of UBI programs offered to consumers will grow quickly.

With this sudden and significant shift toward UBI in the auto insurance marketplace, it will become increasingly important for companies to determine their UBI strategy. Pinnacle Actuarial Resources, Inc. recently announced a business alliance with Driveway Software, to offer UBI analytics and driver behavior scoring for insurance companies.

Pinnacle’s relationship with Driveway will provide assistance to insurers developing a UBI strategy in several ways.

- With over 500 million miles of collected driver behavior data from Driveway’s smartphone app, Pinnacle will be able to develop driver behavior scores that can be used by insurers who want to launch a UBI product but do not have data to develop driver scores and associated rates. These scores will be easily customizable to insurer specifications.

- Pinnacle’s analytics and insurance expertise will help companies translate the driving behavior data into appropriate discounts.

- Combining the driving scores with our extensive customer research will help companies in the development of a strategy that can be employed for increasing the likelihood of success upon launch.

- Partnering with Driveway provides customers with an option for launching a UBI program in less time and at a lower cost than has been possible in the past.

UBI is here to stay, and Pinnacle is excited to be able to offer these services to our customers to help them take advantage of all the benefits a UBI program can bring. If you are interested in discussing UBI services, please contact Roosevelt Mosley at [email protected].

11

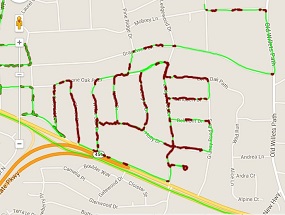

Feb 2015Smartphone LOVE and Usage Based Insurance Implications

With Valentine’s Day around the corner, there’s never been a better time to talk LOVE … in this case, our love affair with electronic devices and apps. While we all know Americans are obsessed with their smartphones, the latest data is juicier than an episode of “The Bachelor.”

With Valentine’s Day around the corner, there’s never been a better time to talk LOVE … in this case, our love affair with electronic devices and apps. While we all know Americans are obsessed with their smartphones, the latest data is juicier than an episode of “The Bachelor.”

Check out these sizzling trends …

- Hotter than husbands? According to January 2014, Pew Research, 44% of cell owners sleep with their phones by their beds and 29% describe their cell phone relationships as “something they can’t imagine living without.”

- Trading up? In 2014, for the first time, people began to spend more time in smartphone apps than watching television! Yes, you heard right. There was a 9.3 percent rise in just nine months. This is a continuing trend, as mobile web usage has already overtaken the PC.

- Speed dating? In fact, in 2012 the iPhone app Draw Something broke Facebook’s record, reaching one million users in just nine days! Mobile advances are reaching consumers at a simply ridiculous rate.

The key to lasting relationships …

- According to this WebDAM infographic, 85 percent of users prefer mobile apps to mobile websites, and yet only 45 percent of U.S. mobile marketing campaigns employ app downloads.

- In the United States, 224 million people actively use apps on their smartphones.

- On top of that, 61 percent of customers report a higher opinion of companies that offer a good consumer experience on mobile.

- As of last year, only 20 percent of CMOs used social media to engage with their customers, but 94 percent of them plan to implement strategies which include mobile apps.

- Forbes reports that mobile is the key to create a sustained relationship with customers. Mobile is increasingly becoming the platform of choice for not only social networking, but contacting customer service.

A formula for successful UBI matchmaking …

Smartphones are driving technological advances and changing UBI policy adoption figures. In 2013, a pilot program conducted in Sweden led to new customers and the transition of existing customers to a UBI program. The article outlines several key points:

- Smartphone telematics will be relevant for several years to come.

- As a UBI alternative, smartphone technology could disrupt contemporary business practices in the insurance industry through technological innovation and improved end-user experience.

- Despite its challenges, smartphone telematics offers a scalable, user friendly alternative to UBI and could result in innovations in the sales process.

Fairytale ending …

While the rest of the usage based insurance story is left to be written, it’s clear that the leading characters are destined for auto industry greatness. America already has a love affair with smartphones, apps and saving money. Auto insurers who appeal to these preferences with smartphone UBI programs can look forward to many years of “automonial” bliss.

Wondering if your policyholders will LOVE smartphone UBI? See it through their eyes in the video below:

09

Feb 2015Auto Insurance Underwriting: Please Mr. Postman – Tell Us How and Where You Drive

Like the lyrics in a Beatles song, auto insurance underwriters are often left waiting and hoping – not for mail, but for accurate information. They wish their policyholders would be forthcoming with truthful information. Unfortunately, that’s usually not the case.

Like the lyrics in a Beatles song, auto insurance underwriters are often left waiting and hoping – not for mail, but for accurate information. They wish their policyholders would be forthcoming with truthful information. Unfortunately, that’s usually not the case.

The image you see above represents a driving route revealed by usage based insurance tracking. This driver’s auto insurance underwriter has no idea that he is driving a delivery route every morning at 3 a.m. He then returns home for most of the day, before leaving to commute to his local community college at 4 p.m. He returns home most evenings at 8:30 p.m.

Harmless right? Not necessarily. It turns out that if you’re an auto insurance underwriter, what you don’t know will hurt you. In fact, this person is not only using his vehicle for a work-related function, he is also driving during the highest risk times of the day.

A 2012 study by the Insurance Institute for Highway Safety found that 32 percent of crash deaths occurred between the hours of 3 p.m. and 9 p.m. Usage based insurance can help you underwrite for high risk drives times in two ways. First, by communicating that high risk drive time has a pricing impact upfront, high risk drivers would not elect to participate and those with low risk drive times will self-select. Second, if there are people in your UBI program who drive during high risk times, you will be able to identify them and price them appropriately upon renewal with the help of accurate driving data.

Zip codes are another common source of soft auto insurance fraud. A carinsurance.com survey found that while the average cost for a 40-year-old man to insure a 2014 Honda Accord was $1,231, a policy with identical provisions could cost as much as $5,109 in some zip codes. Think people in those zip codes enjoy paying five-times the rates? Think again. A fair percentage most likely falsify their garaging addresses … maybe even the postman we’ve been discussing.

Looking at the big picture, insurance fraud costs U.S. insurers $80 billion a year, according to the Coalition of Insurance Fraud. Some of that fraud is soft and some is much more overt. In fact, the organization’s 2015 Fraud of the Month features the “Crash-Gang Dispatcher” – a humble taxi dispatcher who moonlighted as an insurance fraud organizer, sending cronies to maneuver more than 30 staged vehicle crashes. Similarly, Insurance News Networking details the seven worst instances of fraud in 2014 – two of which impacted the auto insurance industry – a legal/chiropractic team that “manufactured” auto injuries and the purposeful sinking of a Bugatti.

While the postman song has a catchy chorus, the message is a bit passive. Auto insurance underwriters simply cannot afford to wait and hope for accurate data. They need a better way of detecting and eradicating insurance fraud. Is usage based insurance the answer? Quite possibly.

For more on usage based insurance’s impact on fraud, click here. To learn more about our UBI pilot program, available to select insurers, contact us.

03

Feb 2015Debunking the “Disinterested” Usage Based Insurance Myth

Over the past couple of weeks, I’ve seen a few articles in the news saying that half of Americans aren’t interested in usage based insurance. They seem to be inferring that the usage based insurance trend is losing demand. Really?

Over the past couple of weeks, I’ve seen a few articles in the news saying that half of Americans aren’t interested in usage based insurance. They seem to be inferring that the usage based insurance trend is losing demand. Really?

This conclusion struck me as a little premature. First, I think we can all agree that most consumers don’t even know what usage based insurance is yet. The technology is in its infancy, with most carriers not even offering it yet. Is it possible that consumers are losing interest … before most even had interest?

Before we jump to conclusions, let’s take a moment to dissect the facts:

Half empty vs. half full. Just last week, we ran an article and an infographic highlighting a 2014 LexisNexis study that concluded that one in three consumers are interested in mobile usage based insurance. I personally felt that interest from one in three consumers was great, especially considering that a lot of consumers don’t really understand UBI yet. I guess you could say my glass was a third full.

The new study from Insurancequotes.com concludes that 49 percent of consumers would not consider usage based insurance. Maybe their glass is half empty? Flipping those numbers, and considering the margin of error in any survey, you could easily say that roughly half of consumers would consider usage based insurance. And that’s a number worth noting.

Risk vs. return. With all products and services, there is a pro and con. For example, the pro of buying a new $350 ski jacket is that you’ll be warm through the winter. The con? You won’t have $350 anymore. A person’s likelihood of buying a $350 ski jacket entirely depends on circumstances. For example, if I ask a Texan, “How likely are you to buy a $350 ski jacket?” she will probably say “not likely.” However, if she was planning a trip to Colorado in two weeks, her answer would probably change.

Now let’s apply this elementary logic to usage based insurance. If you ask consumers if they would consider purchasing usage based insurance, obviously, there’s a downside. They have to give up some degree of privacy. Again, the likelihood of adoption depends entirely on the circumstances – specifically the strength of the upside. The LexisNexis study we highlighted last week, found a positive correlation between the degree of discount offered and consumers’ degree of interest. When the discount level was increased from 5 to 15 percent, consumer interest doubled!

Awareness vs. interest. Finally, anyone who has any experience in marketing knows that before you can get to interest, you have to cross the awareness hurdle – something the usage based insurance segment hasn’t even tackled yet. The insurancequotes.com report cites privacy as a major UBI barrier among older consumers, and goes on to say that many believe their insurers will be able to tell if they’ve been drinking and driving. Anyone detect an awareness issue?

The bottom line: Take a close look at the numbers, and I’m sure you’ll agree … it’s way too early to say that interest in usage based insurance is declining. In fact, interest may be increasing. When all the facts are on the table, and consumers clearly understand exactly what UBI programs monitor, how much UBI programs cost, and how UBI might translate to increased safety, fewer accidents and lower rates, then we can talk.

Want to know more about how usage based insurance can work for your company? Watch the video below.

26

Jan 2015Consumers’ UBI Privacy Concerns Take Back Seat to Safety Needs

In last Tuesday’s blog we told you that 1 in 3 consumers are interested in usage based insurance.

In last Tuesday’s blog we told you that 1 in 3 consumers are interested in usage based insurance.

Today we’re discussing their concerns about consumer data privacy. How many people are wary about privacy? How could these concerns affect your usage based insurance rollout? What can your company do to alleviate privacy concerns and earn usage based insurance business?

Again, we turn to 2014 LexisNexis research for answers to these questions. The company’s findings, compiled from 2,000 respondents, reveal some interesting insights about the future of usage based insurance.

For example, the report predicts that 20 to 30 percent of the insurance market will be captured by usage based insurance within the next five years. And, data indicates that consumers like the idea of insurance controlling costs through safe driving habits. Up 12 percent from 2013, parents are more interested than ever in tracking their teens’ whereabouts and knowing how well their kids are driving. Almost half (45%) of the respondents expressed interest in using UBI data to track the driving habits of family members.

It appears that the high priority of safety may move the privacy issue to a back seat. In other words, consumers may be willing to give up some information in exchange for the opportunity to help themselves and their teen drivers avoid accidents.

While many consumers take issue with giving information to their auto insurance carriers, an equal number are as comfortable with the data exchange as they are with social media. In particular, younger drivers are more accustomed to trading personal data privacy to gain the benefits of technology.

The history of online banking reminds us that consumers will be wary and voice concerns over privacy but convenience and value added services will win out in the long run. Likewise, as consumers become more familiar with usage based insurance, they will acclimate to the data tracking aspect of the product. Case in point: Only 68 percent of consumers in 2014 feel that usage based insurance provides too much information to insurance companies, compared to 72 percent in 2010.

For consumers who are still hesitant around the issue of privacy, insurers can offer value-added services to emphasize the safety benefits of data collection. Providing emergency response and roadside assistance services along with stolen vehicle tracking and recovery are solid counter measures to consumer reluctance. Focusing on teen safety and accident reduction through coaching is also a smart strategy.

Clear communication about the type of data collected is also important. For example, some consumers believe that insurers would be able to tell if they’d been drinking and driving in a UBI program. Of course, insurers can’t detect drinking and driving with smartphone UBI, but nevertheless, it is a concern that needs to be addressed with clear and proactive communication.

Our conclusion: Privacy is still a potential barrier to consumer adoption of usage based insurance, particularly with older audiences. That said, it’s not a formidable barrier. With increased awareness, education and focus on the safety upsides of data sharing, privacy issues will take a back seat. The most important thing that auto insurers can do is to start planning UBI program rollouts, and communicating coming options to policyholders now. The grass is always greener, and policyholders won’t stay with you just because they’re satisfied with your service. Use UBI as a tool to build the relationship and earn their loyalty.

We have limited UBI pilot programs available. Let us know if you’d like to be considered.

20

Jan 20151 in 3 consumers interested in mobile usage based insurance

A quick review of the 2014 usage based insurance study by LexisNexis calls to mind three key words: YOUTH, DISCOUNTS and SMARTPHONES. Want to know more? See notable study conclusions and the full infographic below.

A quick review of the 2014 usage based insurance study by LexisNexis calls to mind three key words: YOUTH, DISCOUNTS and SMARTPHONES. Want to know more? See notable study conclusions and the full infographic below.

Notable finding #1: The under-25 crowd is interested.

In fact, interest in usage based insurance from 21 to 25 year olds jumped from 31 percent to 45 percent between 2013 and 2014, whereas overall awareness only increased by 1 percent, to 38 percent in 2014.

The survey reported that respondents were just as comfortable sharing UBI data as social media, smartphone, and online search data. Autoblog.com reported similar results, and drew connections between receptiveness to UBI and comfort with mobile technology and social media. Young drivers voluntarily post their information using social media already, making privacy less of a concern – especially in the face of the potential savings.

Notable finding #2: Degree of discount drives the degree of interest.

LexisNexis reported that more people are interested in usage based insurance at lower discount rates. The difference between a 5 percent and 15 percent discount doubled interest in usage based insurance among respondents. While 30 percent expressed interest at a 5 percent discount level, a whopping 63 percent showed interest when the potential discount was increased to 15 percent! The addition of value services such as roadside assistance further increased demand.

Notable finding #3: Mobile interest is accelerating.

The study revealed that a great number of people who are responsive to usage based insurance would also be comfortable using apps on their smartphones to monitor driving. The number has increased by 10 percent since 2013, which means that more than one in three consumers now shows interest in mobile UBI.

Smartphone UBI + millennial market + discounts = winning opportunity

Looking for a winning opportunity? Offer millennial clients the chance to receive discounts by enrolling in smartphone UBI. Young drivers are increasingly interested in usage based insurance, and sharing information is less daunting on mobile devices, which they already use for sharing via social media. Engage the smartphone users where they are: on their smartphones.

Well-informed consumers will soon be choosing auto insurers that allow them to save money via smartphone telematics. Are you ready to meet their needs? If not, here’s how you can catch up quickly without having to eat an elephant!

14

Jan 2015The Dollars and Sensors Impeding IoT and UBI Adoption

Most people agree that the Internet of Things (IoT) is exciting, but we still have huge obstacles to clear. These obstacles include how to manage consumer privacy; cybersecurity; and the proficiency of inter-device communication. However, today, I’m not going to talk about any of those hot issues. Instead, I’m going to talk about another massive barrier: The cost of device and sensor management.

Most people agree that the Internet of Things (IoT) is exciting, but we still have huge obstacles to clear. These obstacles include how to manage consumer privacy; cybersecurity; and the proficiency of inter-device communication. However, today, I’m not going to talk about any of those hot issues. Instead, I’m going to talk about another massive barrier: The cost of device and sensor management.

Case in Point: In a blog for Insurance Networking News, Matt Manzella says, “As with most new technologies, the cost of individual sensors is still relatively high, but what makes the cost of the smart home beyond most people’s reach is, to truly have a connected home, one requires a large number and variety of sensors. These may include the following sensors: open/close, motion, cameras, outlets/plugs or switches, water/humidity, temperature, smoke, and may also include things like smart appliances and water shut off valves. A minimal set up could be accomplished for $300-$400, but full coverage in a modest sized home could run $1,000-$3,000.”

Manzella is referring to the cost of sensors for each individual homeowner. But take that a step further. What is the cost of those sensors for each of the companies supplying them?

For those who manufacture connected products, device cost is expected to decline dramatically in the coming years and standardization occurs. However, for service industries that need to be connected without having a manufactured product (think insurance) the cost goes far beyond the physical cost of the sensor. This hardware also has to be procured, inventoried and shipped. And, there’s a wastage cost for sensors that are shipped and lost, or never actually installed by the recipient. At least that was the case for auto insurers that deployed hardware-based UBI rollouts.

In a 2014 Insurance Journal article, written by the Casualty Actuarial Society, Jim Weiss of FCAS shared a hypothetical example in which the UBI dongle cost $100 with a shelf life of three years. In addition, it communicates with the insurer via wireless which costs about $5 a month. He concluded that in this scenario, the insured’s loss ratio would have to drop by 22 percent to justify a permanently installed dongle.

It’s easy to see how hardware can inflate the cost of a usage based insurance rollout and complicate the task of achieving a return on investment. And, that’s just the beginning of the process. At some point, sensors will need to be updated or replaced. To save money, some insurers have considered giving UBI hardware devices to policyholders for only six months at a time, but there are still shipping and inventory issues – not to mention inconvenience to policyholders.

One thing is for sure: Mobile devices are easier to manage than hardware sensors.

Easier management, program scalability, and lower costs are just a few of the reasons that usage based insurance pioneers are making the move to smartphone-based UBI platforms. By delivering usage based insurance via a smartphone app + cloud, insurers can avoid all the hardware hassles. They can deliver usage based insurance instantly by sending the policyholder a link to the insurer-branded downloadable app. And, they can universally update their programs by releasing a new version of the app – without having to manage individual sensors.

Think your company is too small to succeed with usage based insurance? Think again. There are three major developments making UBI more accessible to insurers of all sizes. Also, make sure to download our free report, “10 Reasons to UNPLUG and UNBURDEN your UBI program.” Think you can afford to wait? Studies show that early adopters grow faster. Why not take the lead and let your competitors eat some UBI dust?

08

Jan 2015Usage Based Insurance Helps New Drivers Avoid 40% of Crashes

There’s some interesting new research out from UK-based auto insurer, ingenie. Their Young Driver’s Report revealed that 40 percent of new driver crashes could be avoided with wider adoption of “blackbox” or usage based insurance.

There’s some interesting new research out from UK-based auto insurer, ingenie. Their Young Driver’s Report revealed that 40 percent of new driver crashes could be avoided with wider adoption of “blackbox” or usage based insurance.

While the infographic below fully illustrates the company’s findings, here are a few highlights:

- One in five young drivers crash within their first six months on the road.

- More than 90% of those using usage based insurance, engage with driving behavior feedback and check their feedback 14 times a month, on average.

- Young drivers who share driving feedback with their parents or guardians are 28% less likely to crash than those who don’t.

- Drivers with higher driving scores are less likely to have serious crashes than those with lower scores.

- With ingenie’s usage based insurance program, one in eight drivers crash within their first six months on the road (compared to the usual one in five).

It makes sense that coaching teen drivers should improve their safety and ability to avoid accidents, and now ingenie has the numbers to prove it! In addition, we know that young drivers are digitally engaged, and therefore highly likely to embrace smartphone UBI.

American auto insurers – now is the time to take action. If you haven’t already done so, read this article on how to feed the usage based insurance elephant.