Auto Insurance Underwriting: Please Mr. Postman – Tell Us How and Where You Drive

Like the lyrics in a Beatles song, auto insurance underwriters are often left waiting and hoping – not for mail, but for accurate information. They wish their policyholders would be forthcoming with truthful information. Unfortunately, that’s usually not the case.

Like the lyrics in a Beatles song, auto insurance underwriters are often left waiting and hoping – not for mail, but for accurate information. They wish their policyholders would be forthcoming with truthful information. Unfortunately, that’s usually not the case.

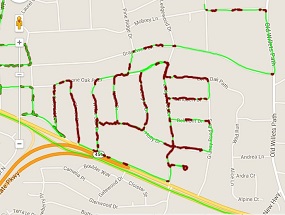

The image you see above represents a driving route revealed by usage based insurance tracking. This driver’s auto insurance underwriter has no idea that he is driving a delivery route every morning at 3 a.m. He then returns home for most of the day, before leaving to commute to his local community college at 4 p.m. He returns home most evenings at 8:30 p.m.

Harmless right? Not necessarily. It turns out that if you’re an auto insurance underwriter, what you don’t know will hurt you. In fact, this person is not only using his vehicle for a work-related function, he is also driving during the highest risk times of the day.

A 2012 study by the Insurance Institute for Highway Safety found that 32 percent of crash deaths occurred between the hours of 3 p.m. and 9 p.m. Usage based insurance can help you underwrite for high risk drives times in two ways. First, by communicating that high risk drive time has a pricing impact upfront, high risk drivers would not elect to participate and those with low risk drive times will self-select. Second, if there are people in your UBI program who drive during high risk times, you will be able to identify them and price them appropriately upon renewal with the help of accurate driving data.

Zip codes are another common source of soft auto insurance fraud. A carinsurance.com survey found that while the average cost for a 40-year-old man to insure a 2014 Honda Accord was $1,231, a policy with identical provisions could cost as much as $5,109 in some zip codes. Think people in those zip codes enjoy paying five-times the rates? Think again. A fair percentage most likely falsify their garaging addresses … maybe even the postman we’ve been discussing.

Looking at the big picture, insurance fraud costs U.S. insurers $80 billion a year, according to the Coalition of Insurance Fraud. Some of that fraud is soft and some is much more overt. In fact, the organization’s 2015 Fraud of the Month features the “Crash-Gang Dispatcher” – a humble taxi dispatcher who moonlighted as an insurance fraud organizer, sending cronies to maneuver more than 30 staged vehicle crashes. Similarly, Insurance News Networking details the seven worst instances of fraud in 2014 – two of which impacted the auto insurance industry – a legal/chiropractic team that “manufactured” auto injuries and the purposeful sinking of a Bugatti.

While the postman song has a catchy chorus, the message is a bit passive. Auto insurance underwriters simply cannot afford to wait and hope for accurate data. They need a better way of detecting and eradicating insurance fraud. Is usage based insurance the answer? Quite possibly.

For more on usage based insurance’s impact on fraud, click here. To learn more about our UBI pilot program, available to select insurers, contact us.